Articles

The Most Useful AI in Small-Business Lending Is Not an LLM

Here is a question we have been working on for a while.

A model is shown the monthly revenue of a small business. Nothing else. Not the owner's credit score. Not the loan it took out last year. Not whether it paid that loan back. Just a sequence of numbers. What came in, month by month, on the platform the business runs on. Trained across hundreds of thousands of these sequences, can it forecast the next twelve months well enough to underwrite the business?

A year of production answered yes. A more interesting answer came with it. The same model, trained only on revenue, never shown a default, turns out to systematically size offers more conservatively for the merchants who go on to take losses. It has no idea what a loss is. It cannot define delinquency. But the way a business's revenue moves contains, it turns out, much of what a credit system spends years learning the slow way. Pipe has been underwriting small businesses embedded in the platforms they run on for years, across five countries and hundreds of thousands of merchants. This is what we have learned by letting a model read the same data we have always read, with sharper eyes. The science is interesting, but what it unlocks is seamless, fast access to capital that traditional financial institutions can't offer, with offer amounts and terms optimized for a business's future, not its past.

Past, present, future

Traditional credit lives in the past. Bureaus read trailing tax filings, prior balances, repayment histories that mature over quarters. Small businesses run in the present. On the platforms where bookings are taken, payouts settle, cancellations land, growth shows up before any of it reaches a credit file. Pipe sits embedded in those platforms, which means we read the present directly. The work is to forecast forward from it accurately enough to put capital in a merchant's hands before the rest of the credit system has even seen the quarter close.

For as long as we have been underwriting small businesses, the best a lender could do with revenue data was extrapolate the trailing average. Classical methods like exponential smoothing do this well. They are robust, interpretable, and hard to beat on stable, recurring businesses. But small businesses are not large companies in miniature. They are more dynamic, more seasonal, more sensitive to a single contract or a single product change. A method designed for the average case is slow to recognize a merchant whose recent shape has departed from the average. The cost is not a metric on a dashboard. It is a plumber who cannot hire the next technician. A cafe owner who cannot add the second espresso machine before peak tourist season. A boutique that cannot front the inventory for a busy quarter.

The reverse failure matters just as much. A forecaster that over-reads a spike, or extrapolates a temporary tailwind into a trend, hands a merchant an offer they cannot support. The graveyard of well-meaning algorithmic credit is full of models that confused a moment for a trajectory — Zillow's iBuying business is the headline example, but the same failure mode shows up in every credit system that mistakes recent noise for a new normal. Forecasting small businesses well means catching the merchant who is genuinely accelerating, and not confusing the merchant who just had three good months with one.

What we built and have been using for more than a year is a Temporal Fusion Transformer - internally, we call it PRF-1. At Pipe it powers multi-horizon revenue forecasting. A sequence model in the transformer family, the same architectural lineage that underlies modern large language models, adapted here for numerical time series rather than text as Claude and GPT models do. Its input is a merchant's monthly revenue. Its output is a distribution over the next twelve months: a forecast and a calibrated band around it. The model learns from hundreds of thousands of merchant histories which past months matter most for the months ahead, per merchant, from data, with no hand-coded rules. The architectural choice matters less than what the architecture lets us do, which is the rest of this piece.

What a forecaster learns about credit when it is never told about credit

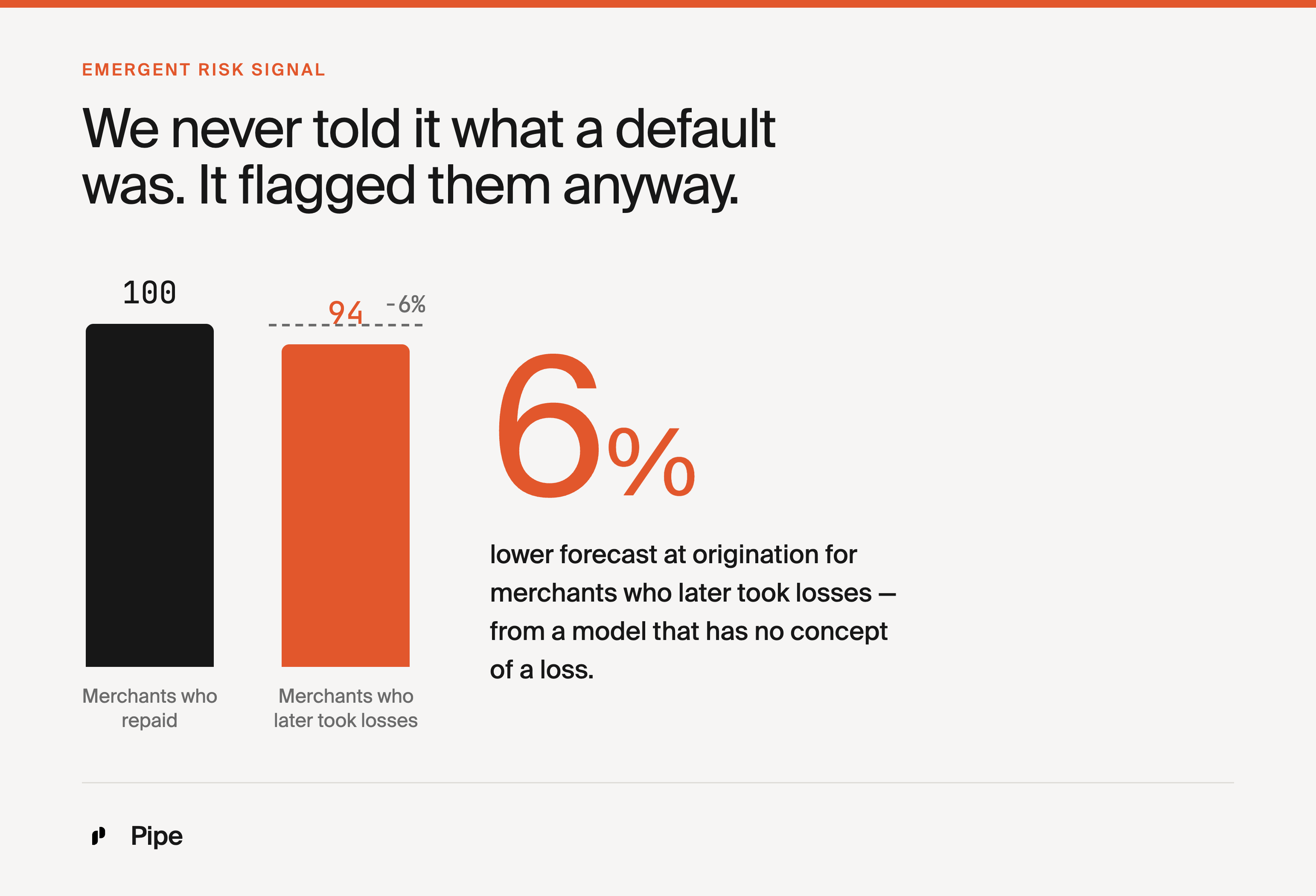

The model has never seen a default. It has never seen a delinquency or a repayment outcome.

The forecasts it produces nevertheless behave like a risk signal. Stratified by repayment outcome, the model systematically sizes offers more conservatively for the merchants who go on to take losses than for comparable merchants who do not. That is without ever having been shown which is which. On the cohort from our first production deployment, the model's forecast at origination ran 6% lower for merchants who later took losses than for comparable merchants who did not. A model that reads cash flow carefully turns out to be reading much of what a credit underwriter spends years learning to read. Not because the model has any concept of credit, but because the structural features that predict where revenue is going are also, in part, the features that predict whether a merchant can carry an offer.

A clean way to think about this: the model is not predicting default. It is predicting revenue, accurately and with calibrated uncertainty, and the merchants whose revenue trajectories are harder to forecast or weaker to begin with are also the merchants who turn out to struggle with repayment. Good forecasting is, partially and emergently, good underwriting.

This has a direct operational consequence. On a new partner, where we have no repayment history yet, we can underwrite from day one with model-driven offer sizing. The cold-start period that normally takes twelve months of repayment data to close is compressed materially. It is the reason the second-partner cutover in April 2026 launched cleanly rather than cautiously, and it is the most concrete way the model has changed how we onboard new platforms.

Uncertainty is the product

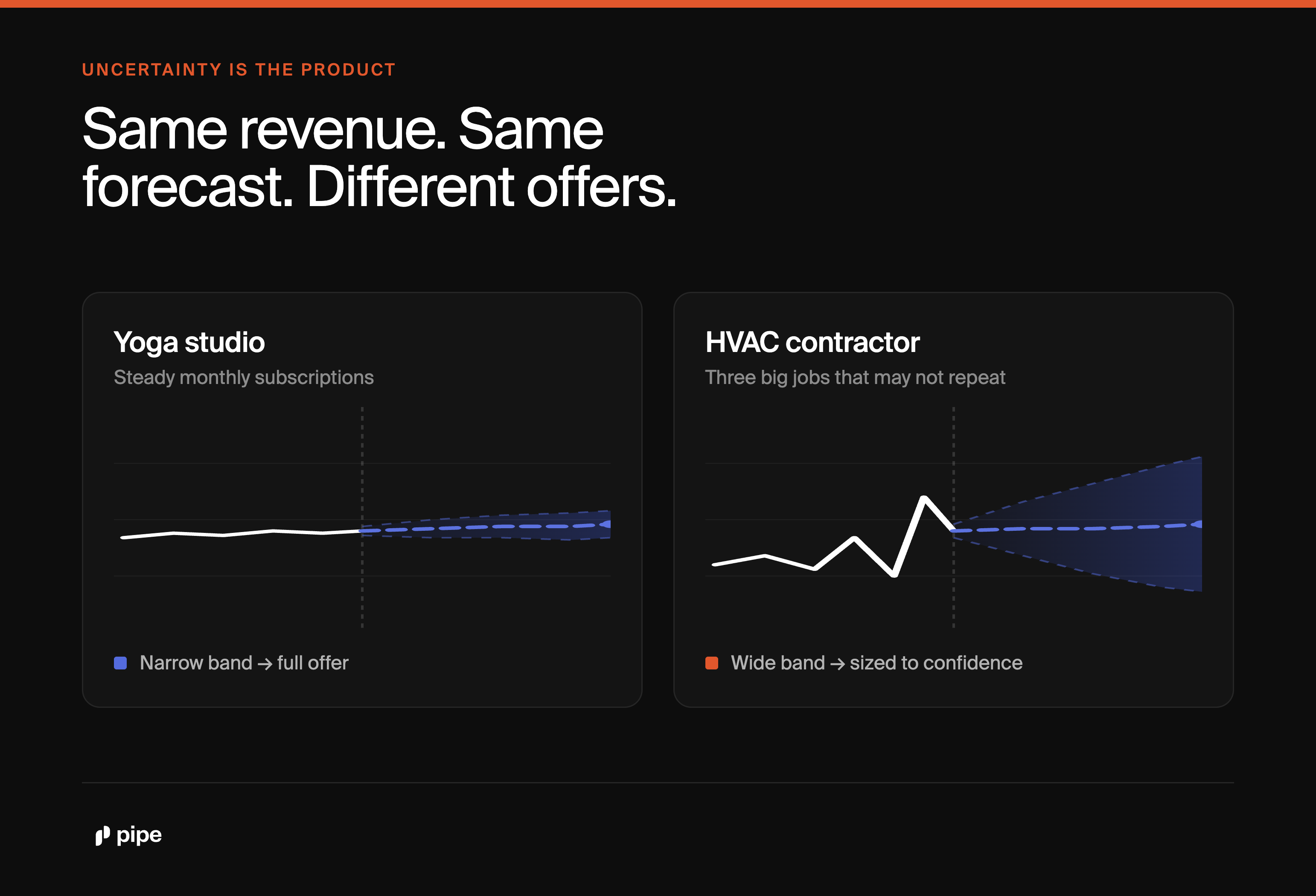

The second most useful thing the model does is not produce a number. It produces a number and a confidence in that number, and the underwriting layer reads both.

Consider two merchants with identical trailing revenue. One is an HVAC contractor who had three large commercial jobs in the last quarter that may not repeat. The other is a yoga studio with steady monthly subscriptions. A trailing-average forecaster gives both the same number. PRF-1 gives both the same median forecast, and a much wider band on the contractor. The underwriting layer reads that width and sizes accordingly. The yoga studio gets the offer their business has earned. The contractor gets one their business can support if those jobs do not come back.

This is the part of the system that took the longest to get right and matters the most. Accuracy is what most forecasters compete on. Calibrated uncertainty is what changes how you can use a forecast. It is the difference between a model that tells you what it thinks will happen and a model that tells you how much to bet on what it thinks will happen. For SMB credit, where the cost of being wrong is asymmetric. A too-large offer creates repayment stress, a too-small one leaves a growing merchant under-capitalized. Sizing capital to confidence is the actual product innovation.

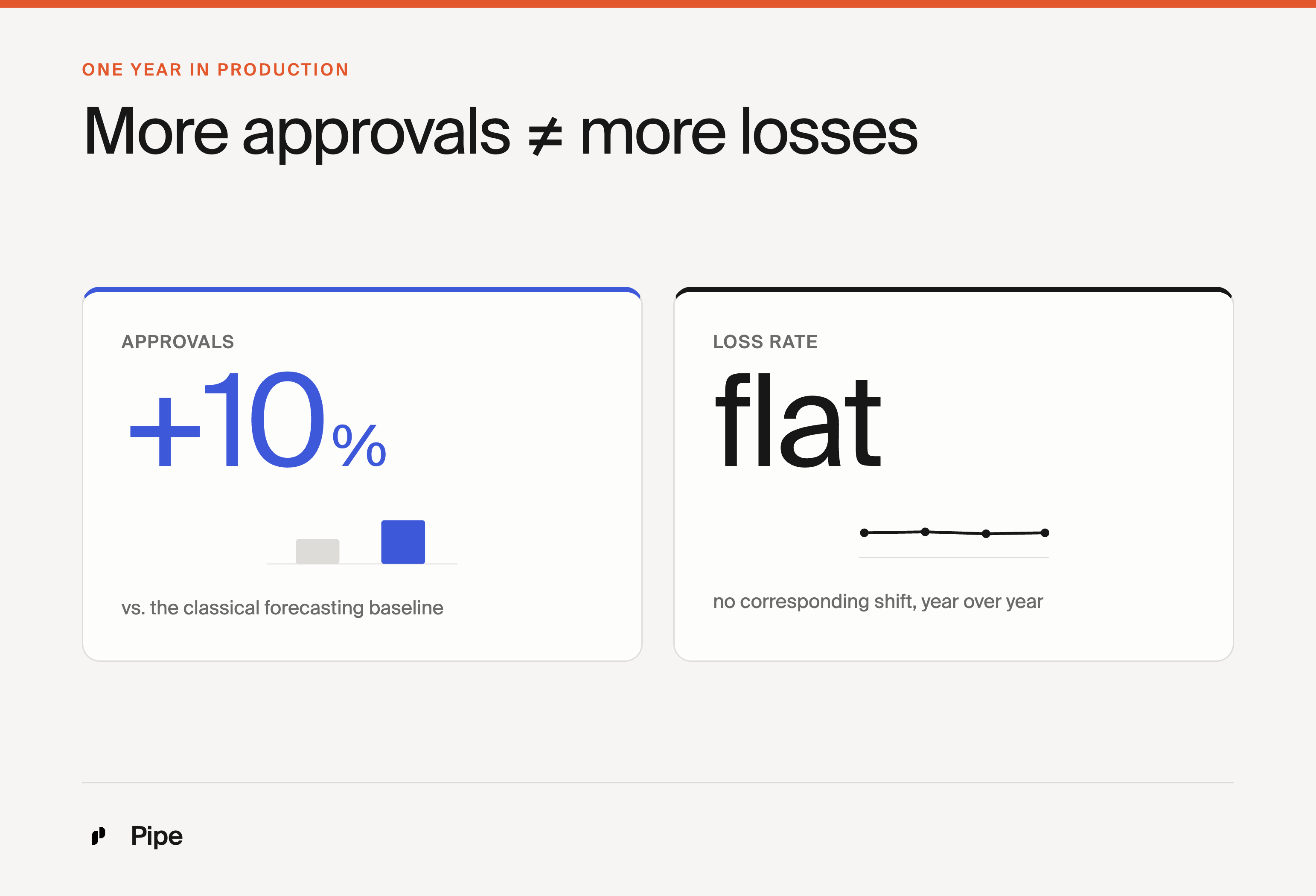

A year in, the model-underwritten book has expanded approvals 10% relative to the classical forecasting baseline, without a corresponding shift in loss rates. The merchants who benefit most are the ones a trailing-average forecaster systematically under-reads. The merchants who would have been over-extended under a less confident model get offers their business can actually carry.

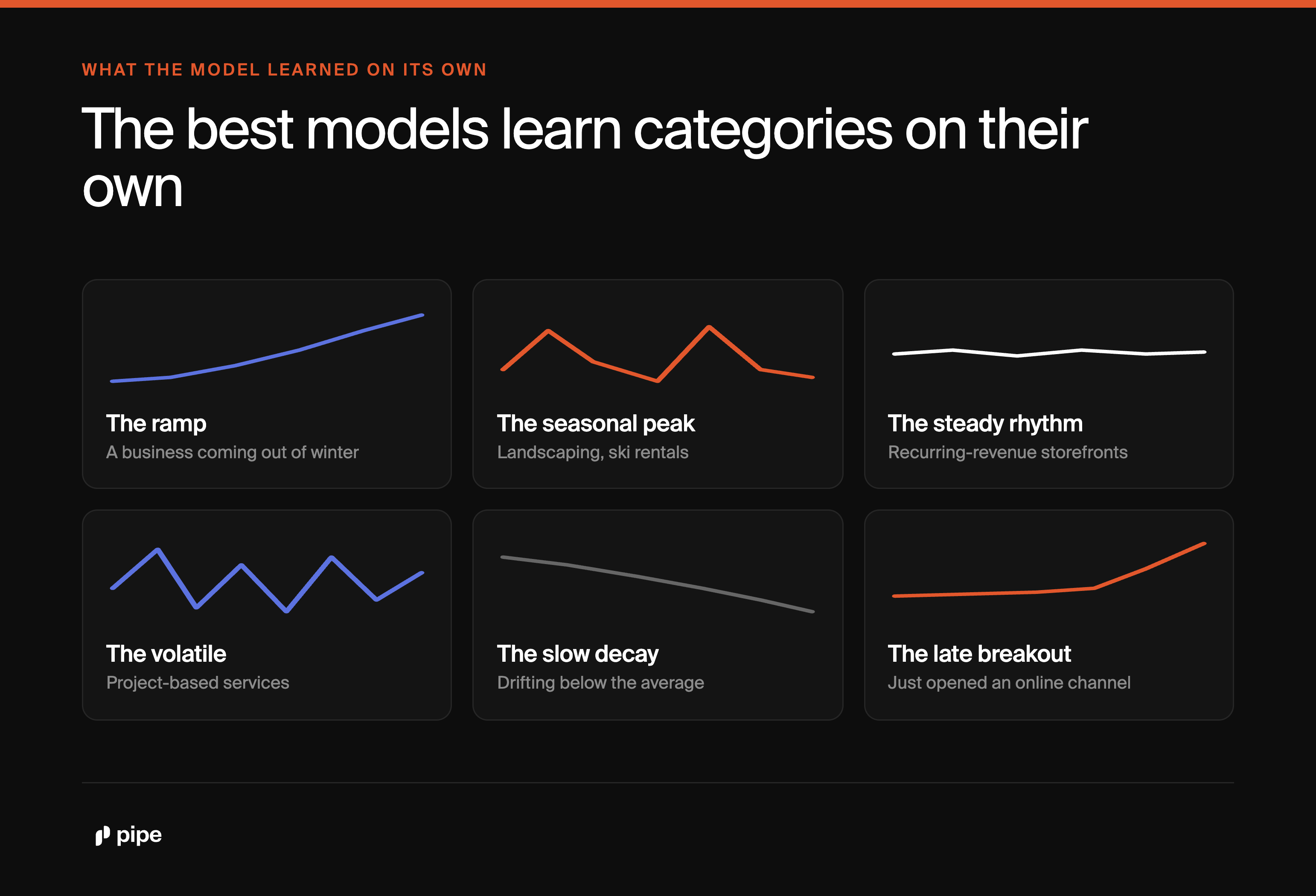

What the model learned about small businesses

Merchant revenue has a grammar of its own. Recent months can dominate the near-term forecast. Same-season periods can matter when a business has enough history. A spike can be meaningful for one merchant and noise for another. A flat trailing average can hide a business that is slowly decaying or slowly accelerating. Some merchants read like a steady rhythm. Others like a long crescendo. A forecaster trained across hundreds of thousands of these histories learns to read both.

Archetypes emerged on their own, and we now use them.

PRF-1 was never told that landscaping and ski rentals are seasonal, that recurring-revenue storefronts behave differently from project-based services, or that a ramping business looks structurally different from a volatile one. It learned these categories from data, with no human supervision calling them out. And within each archetype, finer variations: a seasonal merchant whose peaks grow larger each year is not the same as one whose peaks are flat; a volatile merchant can look seasonal at a glance and behave very differently. The vocabulary the model produced is now the vocabulary we use when we talk to partners about their merchant base. It changed how we describe what we underwrite, not just how we underwrite it.

The model catches growing merchants earlier.

Classical methods are built to be cautious. They wait for evidence before extrapolating a trajectory. That is correct for most merchants and structurally too slow for the ones scaling fastest. A model that has seen enough histories recognizes the shape of a ramp before the trailing average catches up — a landscaping crew coming out of winter, a boutique that just opened an online channel, a catering business that just locked a quarterly corporate contract. These are the merchants whose offers now move with their business as it grows, not after it has grown.

What a year in production actually looks like

A model is a claim until it ships. In May 2025 we put PRF-1 into production on one of our largest partner books. The first real read on whether the work would hold up outside a notebook. The harder question is not whether the model performed in aggregate. It is what happens in the cases it gets wrong, and whether we catch them before merchants do.

Monitoring is the part of the work that does not show up in a launch announcement and is the part that determines whether a model is durable. We backtest weekly against held-out cohorts, watch forecast errors by partner, geography, archetype, and tenure, and treat widening uncertainty bands themselves as a leading indicator. When a segment's bands begin to widen before its errors do, the model is telling us something has shifted before we can see what. The small things we caught in the first year were resolved before they touched a merchant offer. The system that catches them is as much of the work as the model itself.

Across the first year, on the model-underwritten book: approvals on growing-merchant cohorts expanded relative to the trailing-average baseline. Loss rates did not. The errors the model does make are balanced; 49.5/50.5 between slight over-forecast and slight under-forecast. Close to an even split between slight over-forecast and slight under-forecast. Which means we are not systematically inflating offers in ways that create repayment stress, nor under-extending in ways that leave growing merchants under-capitalized. The forecast is doing what a forecast is supposed to do: getting closer to the truth, in both directions, in a way the underwriting layer can act on.

That track record is what let us cut over a second major partner in April 2026. The launch was clean. Monitoring was live in week one. Each cutover sharpens the playbook for the next.

Where this goes

Small businesses are the most dynamic credit population in the country, and the least well-served by the systems built for everyone else. Pipe's mission is to expand access to unbiased capital for the merchants the rest of the credit system is slow to see. The platforms that serve those merchants are where that work has to live, close to the present, close to the business, close to the moment the offer matters most.

PRF-1 is one chapter of a longer practice. There is more in a merchant's history than the current version can see, and the science keeps moving. The next phase of the work is less about a better forecast and more about a tighter loop between what the model reads, what it is uncertain about, and what we offer, sizing capital to confidence, at the speed of the platforms where small businesses actually run.

Disclaimer: Pipe and its affiliates don't provide financial, tax, legal, or accounting advice. What you're reading has been prepared for knowledge-sharing and informational purposes only. Please consult your financial and legal advisors to determine what transactions and decisions are right for you and your business.